Most drivers pay an automobile insurance premium every month, but they seldom think about what happens when they need to file insurance claims.

If you’re not sure how to file an insurance claim or how insurance claims work, this is a brief introduction to the topic.

Every traffic accident and insurance claim is unique, so a variety of factors may affect how long the process takes and what you’ll receive when the process concludes.

Understanding your automobile insurance coverage should be a top priority for every motorist in the state of Massachusetts. Understanding your coverage prepares you if a collision happens.

Laws in all fifty states require motorists to notify their auto insurance companies promptly following any traffic collision.

When you make an auto insurance “claim,” you are asking an insurance company to pay for your personal injury expenses and/or the property damage to your vehicle, or any other property damage, sustained in the crash.

WHEN SHOULD YOU NEGOTIATE YOUR CLAIM DIRECTLY WITH AN INSURANCE COMPANY?

After a traffic collision in Massachusetts, if you’ve sustained only vehicle damage, there’s usually no reason why you shouldn’t negotiate directly with an auto insurance company.

If, however, a negligent driver injured you in the collision, before you even speak with an insurance company, discuss your legal rights and options with a trustworthy Boston personal injury attorney.

In some cases, injured victims of negligent drivers will have to file a personal injury lawsuit to be reimbursed for their medical bills and other injury-related losses.

Presented here are some suggestions for negotiating a vehicle damage claim. It’s not a difficult procedure.

The first step is simply notifying your own auto insurance company that you’ve been involved in a traffic crash.

If you negotiate your claim without an attorney’s help, contact the company, complete the claim forms and other paperwork, and include any supporting documentation.

A negotiation usually takes only several telephone discussions and sometimes a short personal meeting with an adjuster.

Before you negotiate with an insurance company, decide what you believe is the appropriate settlement amount, and then determine what is the lowest amount that you are actually willing to accept.

Keep that second amount to yourself.

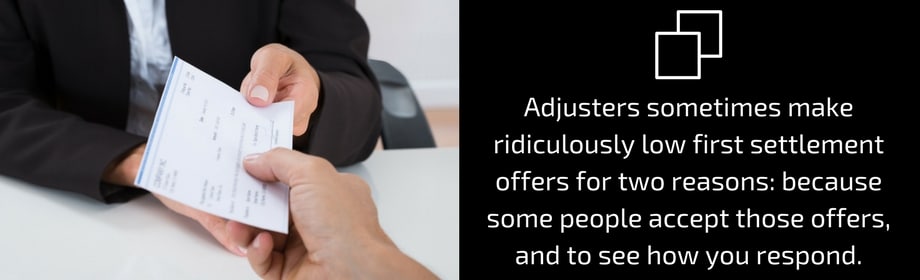

Adjusters sometimes make ridiculously low first settlement offers for two reasons: because some people accept those offers, and to see how you respond.

Your response should be a figure above the adjuster’s first offer and only slightly lower than your own original claim request.

WHAT CAN INSURANCE CLAIMS NEGOTIATION ENTAIL?

You may have to negotiate back and forth several times with the adjuster to reach an acceptable final agreement. Do not be hurried, pressured, or intimidated.

Identify the strongest point of your claim – it might be that the other driver was legally intoxicated, for example, or that your family members have been seriously inconvenienced – and emphasize that point throughout the negotiations.

Verify the final agreement at once and in writing.

Send the adjuster a letter – not an email – confirming the final settlement amount, what that amount covers, and the anticipated date of payment.

The insurance company should make the payment promptly.

Most insurance adjusters and other insurance professionals working in Massachusetts act in good faith to pay claims promptly and properly.

However, if you are negotiating an insurance claim and the company offers you excuses, uses delaying tactics, or fails to pay you promptly after a claim settlement has been reached, you may be the victim of an insurance company’s bad faith.

In this state, a victim of insurance bad faith can seek a legal remedy. Simply obtaining legal counsel may be all that’s needed to get an insurance company to treat you fairly.

If it isn’t, your attorney may recommend that you pursue an insurance bad faith lawsuit. In some states, such as Arizona, you will need the help of an Arizona personal injury law firm.

WHAT IS REQUIRED FOR INSURANCE CLAIMS AT THE SCENE OF AN ACCIDENT?

If you are involved in a traffic accident in Massachusetts, there are several steps you must take at once.

You need to know what those steps are because, at the scene of a crash, you won’t be able to speak to an attorney or an adjuster.

When a traffic accident occurs, see if anyone needs immediate medical attention and if so, summon it.

If you’ve been injured, get treated, but if you aren’t injured, try to get a check-up anyway and within 24 hours if possible. That way, you’ll know if you sustained any latent injuries, and you’ll create the medical records that you might just need as the legal situation after the accident unfolds.

The next task is summoning the police. Ask them how you will be able to obtain their accident report, and when you have it, make several copies.

You’ll need to trade names, driver’s license numbers, and personal and insurance contact information with the other driver, and it’s a good idea to confirm that information as soon as you can.

It’s rare, but sometimes accident victims are given false information and even phony insurance cards.

Take photographs – as many as you can – of the site of the crash and the vehicle damages. If you’ve been injured in a way that’s visible, have someone photograph your injury or injuries.

Finally, if it’s possible, obtain the names and contact information for any eyewitnesses. Photos and eyewitness testimony can be convincing evidence if your claim cannot be settled quickly and a legal dispute emerges.

Be ready to offer all of the information you’ve compiled, as well as your own version of what happened, when you file your auto insurance claim.

Depending on which motorist is deemed “at-fault” for the collision, either motorist’s insurance company might be responsible to pay for repairs.

If the two companies cannot agree on who was at fault or on how much should be paid for repairs, you may need an attorney’s advice.

Again, most of the suggestions offered here apply to property damage in a traffic accident. If you sustained even a minor physical injury in traffic due to another driver’s negligence – anything more than the most trivial small cuts or bruises – don’t even speak with an insurance adjuster, don’t provide anything in writing, and do not put your signature on any insurance documents.

When your health and your future are at stake, let an experienced Boston personal injury attorney – who is also a trained negotiator – handle your claim, protect your rights, and negotiate on your behalf.